Over the past few months, the Canadian government has introduced significant changes to mortgage rules, aiming to make homeownership more accessible. These changes, set to take effect on December 15, 2024, address pain points in the existing system and offer potential solutions for homebuyers, especially first-timers and those seeking new builds.

Timeline and Key Changes:

- August 1, 2024: 30-year insured mortgage amortizations were introduced for first-time homebuyers purchasing new builds.

- September 16, 2024: The government announced further mortgage reforms, with details released on September 24, 2024.

- September 25th, 2024: Uninsurable switches no longer face stress test effective November 21st.

- December 15, 2024: The new mortgage rules, including the increased price cap and expanded eligibility for 30-year amortizations, come into effect.

High Barrier to Entry in Expensive Markets

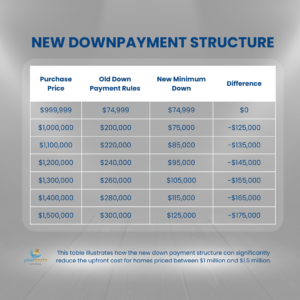

The previous $1 million cap on insured mortgages meant buyers in expensive cities like Toronto and Vancouver often needed a down payment of 20% or more. This made it difficult for many, especially first-time buyers, to enter the market.

The Solution: The government is increasing the price cap for insured mortgages to $1.5 million. This means more buyers can qualify for a mortgage with a smaller down payment (as low as 5% for a portion of the purchase price).

This table illustrates how the new down payment structure can significantly reduce the upfront cost for homes priced between $1 million and $1.5 million.

High Monthly Mortgage Payments

Rising interest rates and the high cost of living made monthly mortgage payments challenging for many Canadians.

The Solution: The government is expanding eligibility for 30-year mortgage amortizations. Previously limited to those with down payments below 20%, this option will now be available to all first-time homebuyers and all buyers of new builds, regardless of down payment size.

How it Helps: A 30-year amortization means lower monthly payments, making homeownership more manageable. However, it’s important to note that this also leads to paying more interest over the life of the loan.

Lack of Flexibility and Competition in Mortgage Renewals

Previously, switching lenders at mortgage renewal often meant undergoing another mortgage stress test. This discouraged competition and could lead to homeowners getting stuck with their current lender even if better rates were available.

The Solution: The government introduced the Canadian Mortgage Charter, which allows insured mortgage holders to switch lenders at renewal without another stress test. This promotes competition and allows homeowners to access more favorable rates and terms.

Impact on the Canadian Real Estate Market

These changes are expected to impact the Canadian real estate market in various ways:

- Increased Demand: Lower barriers to entry and more manageable monthly payments could lead to increased demand for housing, potentially driving up prices.

- Focus on New Builds: The emphasis on 30-year amortizations for new builds might incentivize more construction, addressing the housing shortage.

- Shift in Buyer Demographics: These changes could attract more first-time homebuyers and younger generations to the market.

Pros and Cons for Homebuyers

| Pros | Cons |

|

|

How will you keep track?

Understanding and leveraging these mortgage rule changes can be complex. While the information here provides a basic overview, it’s essential to consult with a professional mortgage broker for personalized advice. A qualified broker can help you navigate these changes, understand your specific financial situation, and find the best mortgage solution for your needs. Reach out today if you have any questions.