Interest rates are a key concern for both current and aspiring homeowners in Toronto. Understanding why mortgage rates are high, whether they will decrease, and what to expect in the coming years can help you make informed decisions about your home financing. This blog will cover the current trends in interest rates, the Bank of Canada’s recent actions, and predictions for the future.

Why Are Mortgage Rates So High?

Several factors contribute to the high mortgage rates we are experiencing:

Economic Conditions

High inflation is a major factor driving up interest rates. To combat inflation, the Bank of Canada raised its benchmark overnight rate to 5.00% in 2023. This increase has directly impacted mortgage rates across Canada, including in Toronto.

Central Bank Policies

Central banks, including the Bank of Canada, use interest rates to manage economic activity. Stephen Poloz, former Governor of the Bank of Canada, noted that central banks adjust rates to either stimulate or cool down the economy. Recent rate hikes have led to higher mortgage rates, affecting homeowners in Toronto. When we adjust our policy interest rate at the Bank, we don’t expect immediate results. It usually takes 18 to 24 months to see the full effects.

Global Economic Uncertainty

Global events and economic conditions, such as geopolitical tensions and economic slowdowns, can drive up borrowing costs. These factors also contribute to higher mortgage rates.

Demand and Supply

High demand for homes in Toronto has pushed up mortgage rates. When more people are looking to buy, the cost of borrowing increases, impacting new and current homeowners.

Are Mortgage Rates Going Down? What You Need to Know

The trajectory of mortgage rates is a hot topic for homeowners and those looking to enter the housing market. Understanding recent trends and future predictions can help you make more informed decisions. Here’s a look at what’s happening with interest rates, the Bank of Canada’s actions, and what you can expect moving forward.

Recent Actions by the Bank of Canada

The Bank of Canada has recently implemented three consecutive rate cuts of 0.25% each. These adjustments reflect a response to the slowing economy and aim to stimulate growth. This series of rate cuts indicates a shift in policy to support economic activity.

Predictions for the Near Future

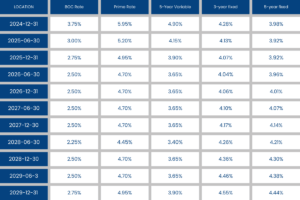

Looking ahead, predictions suggest that further cuts may occur for the remainder of 2024 and into the middle of 2025. However, rates are not expected to return to the historically low levels seen during the COVID-19 pandemic. Instead, the focus is on gradually stabilizing the rates to better align with current economic conditions.

Economic Trends and Central Bank Policies

The Bank of Canada uses interest rate adjustments to manage economic conditions. When the economy slows down, as it is currently, the central bank lowers rates to encourage spending and investment. Conversely, during periods of economic overheating, rates are increased to temper growth. The recent rate hikes over the past two years were aimed at cooling down an overheated economy, but those conditions are largely behind us.

Future Predictions for Mortgage Rates

Gradual Decline Expected

Although rates are unlikely to hit the lows experienced during the pandemic, they are expected to stabilize and form a new norm by 2026/2027. Data trends suggest a gradual decline in rates leading up to this period. This decline will enhance affordability for homeowners, reduce the total interest paid over the life of a mortgage, and make it easier for those waiting to enter the market.

Economic and Global Influences

Economic conditions will play a crucial role in determining future rate adjustments. If inflation remains controlled and the economy stabilizes, further rate reductions might be on the horizon. Additionally, global economic conditions, such as slowdowns in major economies, could influence Canadian rates.